Vansh Sheth

Research Analyst, Capera

Writes sharp essays about banking systems, capital flows, and markets infrastructure.

13 articles published

Articles by Vansh

RBI Just Made Dollar Debt Cheaper Than Rupee Debt. For PSUs.

On 8 June 2026 the RBI opened a fixed 1.5% US Dollar-Rupee swap for public-sector external commercial borrowings of 3-5 years, open only until year-end. That fixes the currency hedge at roughly half the market rate and drops the all-in cost of dollar debt to 6.50-6.75% in rupees, about 75 bps under what a AAA PSU pays in the domestic bond market. The bridge, the traded yields, and who benefits.

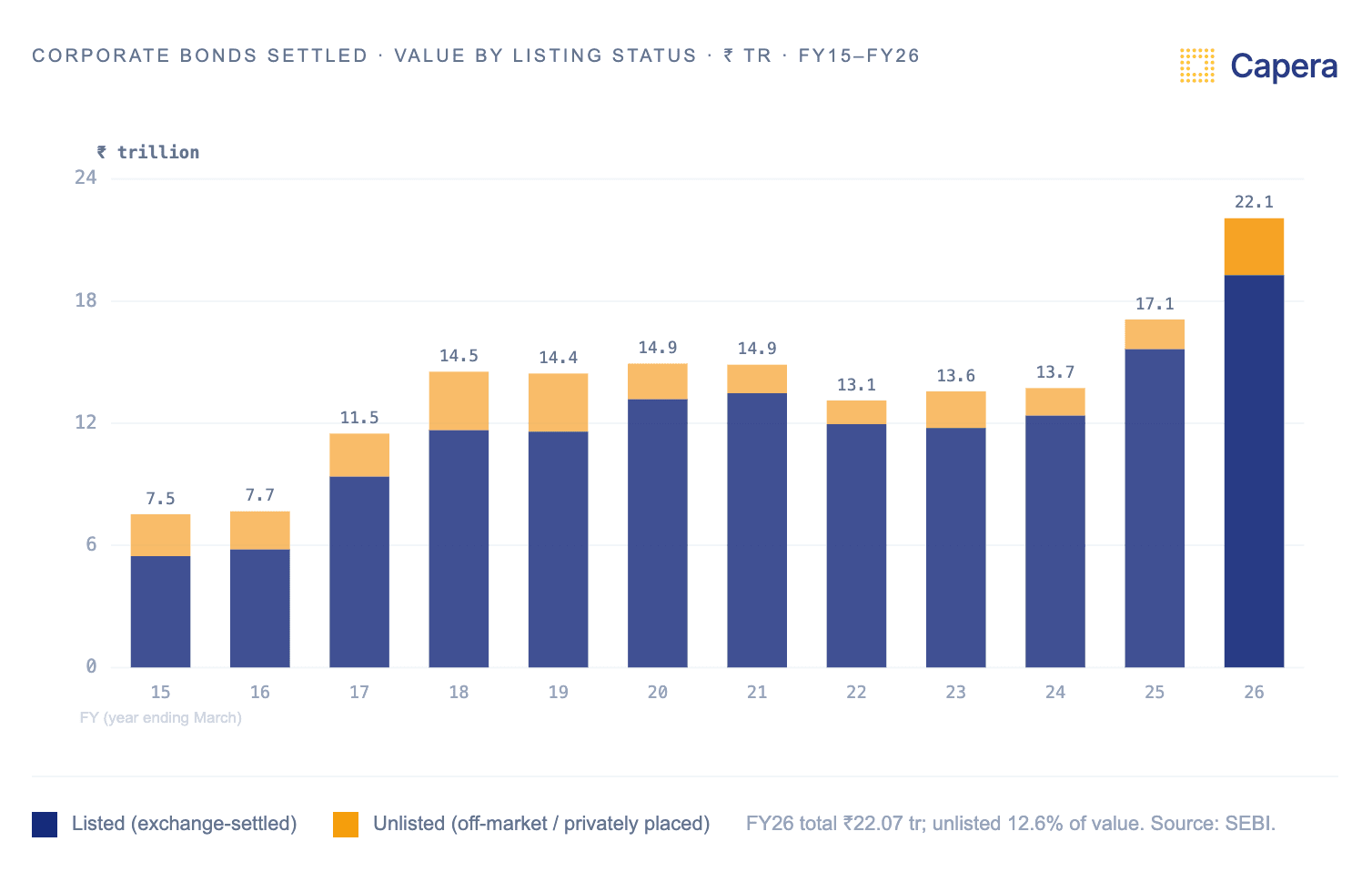

India's Bond Market Just Shifted Into a Higher Gear

India's corporate bond market just had a breakout year. SEBI's settlement data shows 28.4 lakh trades cleared in FY26, up 139%, with value up 29% to ₹22.07 trillion, even as the average ticket nearly halved to ₹0.78 crore. More trades in smaller lots: the market is broadening, and the rails for its next leg are going in. A decade of listed vs unlisted settlement, decoded.

When Short Money Pays More: India's Debt Market in May 2026

India's debt market turned over ₹5.2 lakh crore in May. A liquidity squeeze drove CD yields up ~130 bps to 7.8% while the 10-year G-sec held near 7.0%, flattening the high-grade curve and inverting the front end: short money paid more than a five-year AAA bond. For treasurers, May rewarded staying short and picking credit over duration.

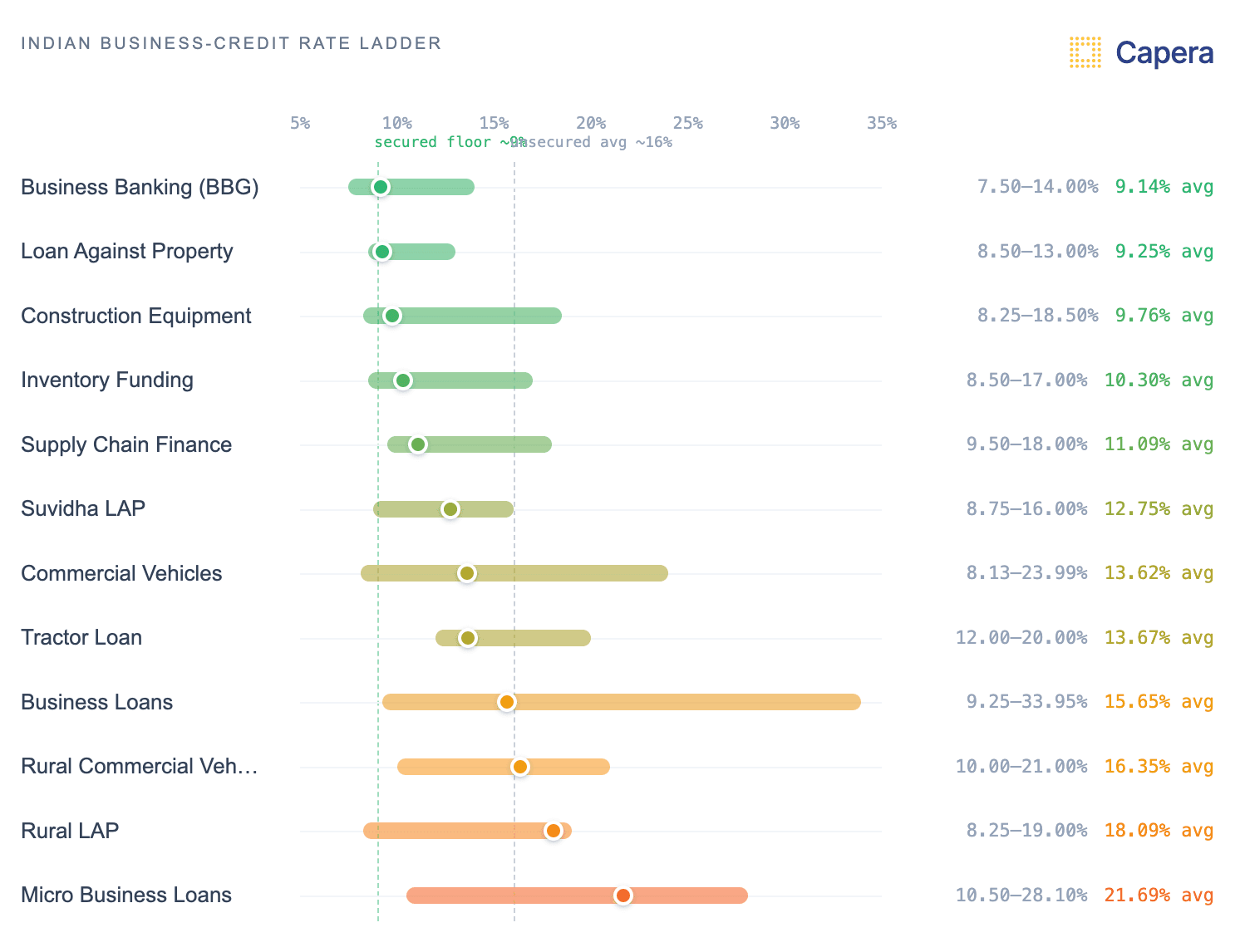

The Real Price of Business Credit: Why Collateral Is Your Cheapest Lever

At one bank, in one quarter, the average cost of business credit ran from 9% to 26%. The biggest thing moving you along that range is not the lender; it is how much collateral you post. A read of the financing ladder, and why sequencing draws collateral-first is treasury work.

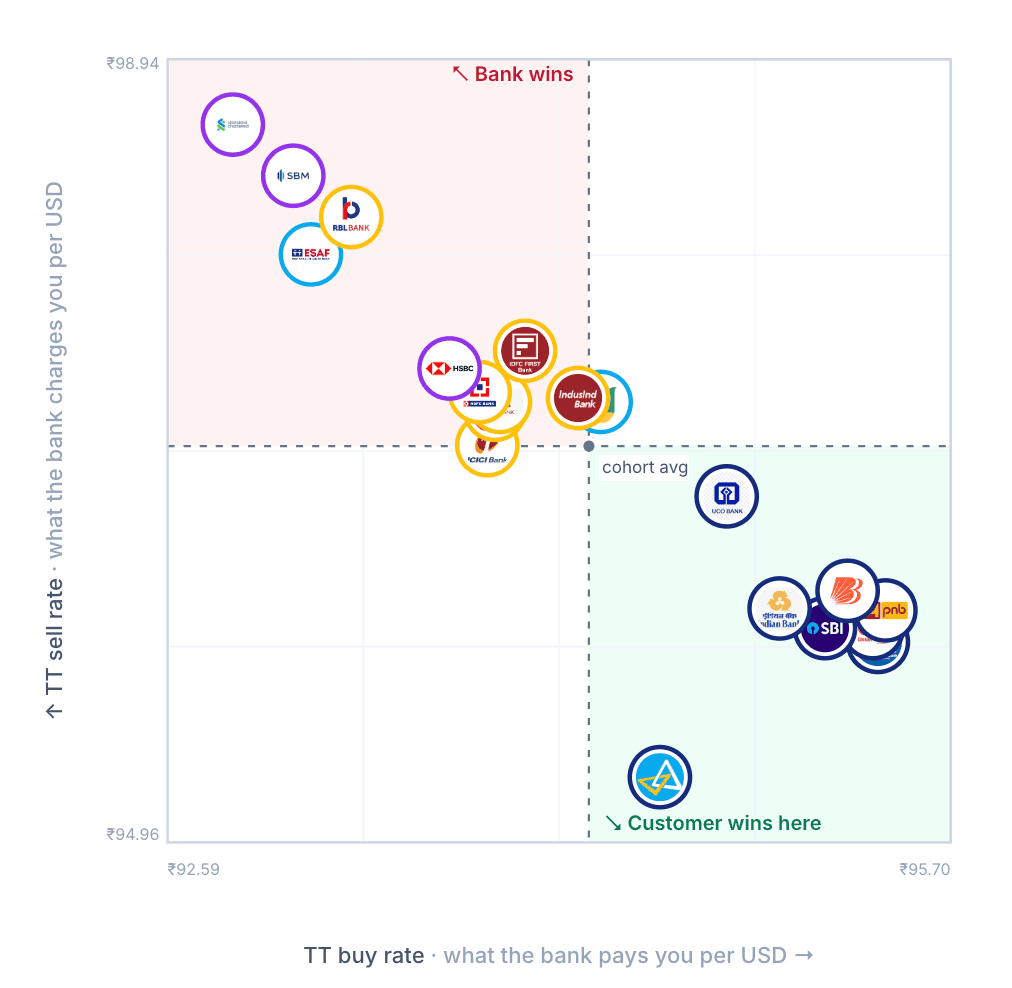

Choose your FX bank carefully. The spread across Indian banks can be 10×.

On the same USD trade, on the same day, the gap between the tightest and the widest Indian-bank quote can span an order of magnitude. Cohort labels — public-sector, private, foreign, small-finance — don't reliably predict who's pricing tight today. The customer-direction view, plotted bank-by-bank, does.

The UAE's $250 Billion SME Funding Gap. And What's Closing It.

UAE SMEs generate 63% of non-oil GDP and receive under 10% of bank credit. The GCC-wide funding gap is roughly $250 billion. A new layer of non-bank capital, partnership lending, e-invoicing, and the Red Sea trade reroute are reshaping how that gap closes. A structural read of where UAE SME finance is heading.

India's Forex Distribution Map Just Got Redrawn: FEMA 401/2026-RB Explained

On 30 April 2026 the RBI notified FEMA 401/2026-RB. FFMC licences sunset, AD Category-II picks up trade and maintenance remittances up to ₹25 lakh per transaction, and a new Forex Correspondent Scheme replaces the franchisee model. The structural changes, what they mean for SMBs, and the market that the rewrite is aimed at.

EBLR vs MCLR: What Changed in 2019, and Why Your Loan Reset

RBI replaced banks' internal cost-of-funds benchmark with an external one for retail floating-rate loans. The mechanics, the borrowers who got moved, the ones who didn't, and what's still priced off MCLR seven years later.

Repo Passthrough: What It Actually Means for Your Home Loan EMI

A 25 bps repo cut does not reach your EMI overnight. How the cut transmits through EBLR, why some banks pass less than the full move, and how to tell if your bank is dragging its feet.

Floating vs Fixed Home Loans: The Trap Most Borrowers Miss

Indian banks rarely sell a true fixed-rate home loan for the full tenure. The reset clause buried in the sanction letter is where the floating-vs-fixed question actually gets answered.

United States Escrow Architecture. 2026 Edition.

A structural analysis of U.S. residential and capital markets escrow frameworks. Comprehensive breakdown of RESPA, Regulation X, and contractual escrow models for institutional investors.

RERA Escrow Architecture in India. 2026 Edition.

A regulatory-circular-level structural deep-dive for institutional investors. State-wise analysis of escrow rigidity, compliance intensity, and capital risk across Maharashtra, Karnataka, Gujarat, Uttar Pradesh, Telangana, and Haryana.

UAE RERA Escrow Architecture, Dubai Focus. 2026 Edition.

A regulatory-grade structural analysis of UAE escrow regulation under Dubai Law No. 8 of 2007. Comparative study of Dubai vs Abu Dhabi escrow systems, milestone-based disbursements, and investor risk modeling.